Three high-value spaces to explore across the mortgage experience –

and how to get started.

Buying a house should be exciting. But across the &us team, recent home-buying experiences felt more like a slog – full of clunky applications, confusing options, and lacklustre remortgaging journeys. Given our bread and butter is innovation, we couldn’t help but ask: how can mortgage lenders make this better?

So, we did some digging.

Despite its current shortcomings, the mortgage industry is on the cusp of a major shift. With AI, automation, and a wave of younger buyers entering the market, long-standing frustrations are finally getting attention. Lenders are tackling everything from faster application processing, to improving portfolio performance and the accuracy of risk projection.

But where to begin?

The future of mortgages is exciting, but for mortgage lenders operating in a heavily regulated space, change can feel daunting. And when every new solution sounds promising, where do you focus?

To help narrow it down, we’ve pinpointed three opportunity spaces that lenders should explore first, along with some bite-size product ideas to serve as food for thought.

The three opportunity spaces

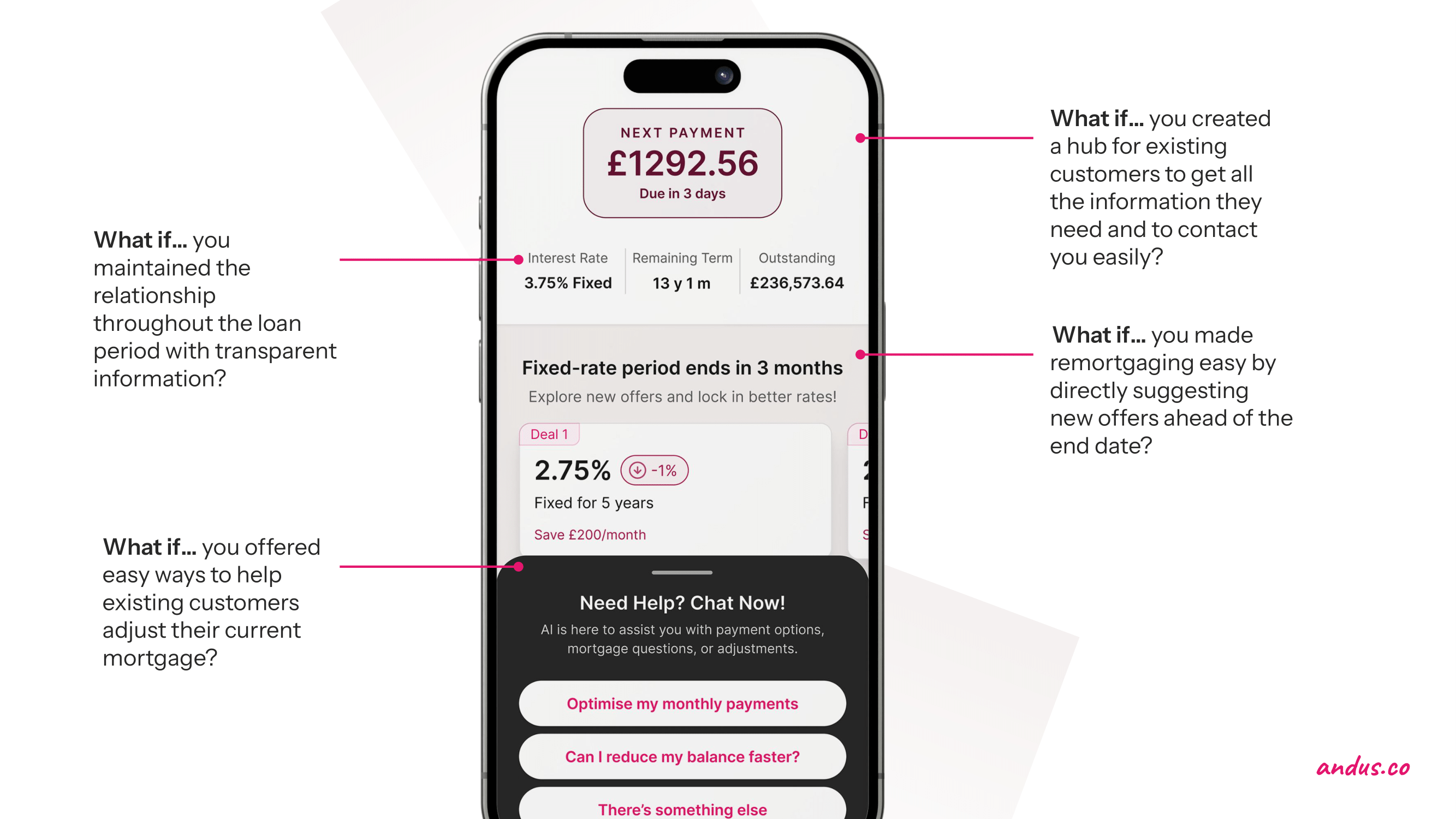

Grow the trust of existing mortgage customers

Deliver a next-level application experience

Seize the power of personalisation

1. Grow the trust of existing mortgage customers

Starting with existing customers makes real sense from a product strategy perspective because it allows you to optimise value from customers you’ve already won. By giving them a first class digital customer experience, you can retain the relationship and unlock greater long-term value.

The problem to solve:

The reality is that the majority of your customers probably came via a broker – making them 2x more likely to switch lenders at the end of their term. In fact, most lenders have very few touchpoints with buyers after the initial application and setup. Some buyers may not even hear from their lender again until it’s time to renew – that’s years down the track. This means valuable opportunities to build deeper, longer term relationships and loyalty are lost.

The big questions:

How can you grow relationships with existing customers, so when the initial term is complete, they renew with you?

How do you get the basics right with a good user experience and simple technology improvements?

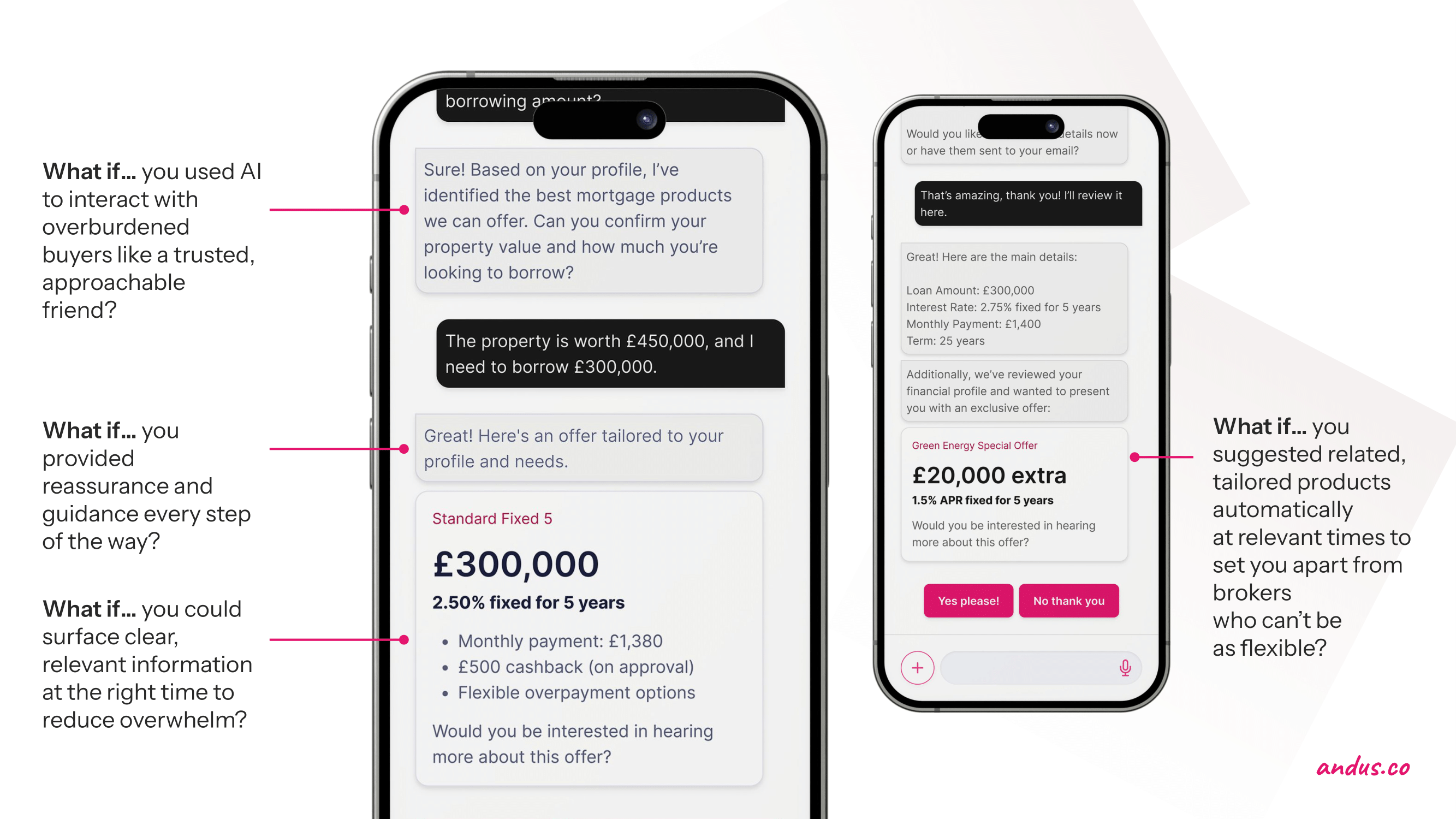

2. Deliver a next-level application experience

Having unlocked more value from existing customers, it’s now time to shift your focus to new applications. Consider how the process can be better, faster and more efficient for new customers and your own teams.

The (customer) problem to solve

The current mortgage process is confusing and stressful for buyers. Not only are buyers bombarded with a high volume of information, most buyers (64%) also don’t have a good understanding of mortgage terminology.

The big question

How could you make the experience of picking a mortgage for customers as simple as picking a contract for their mobile phone?

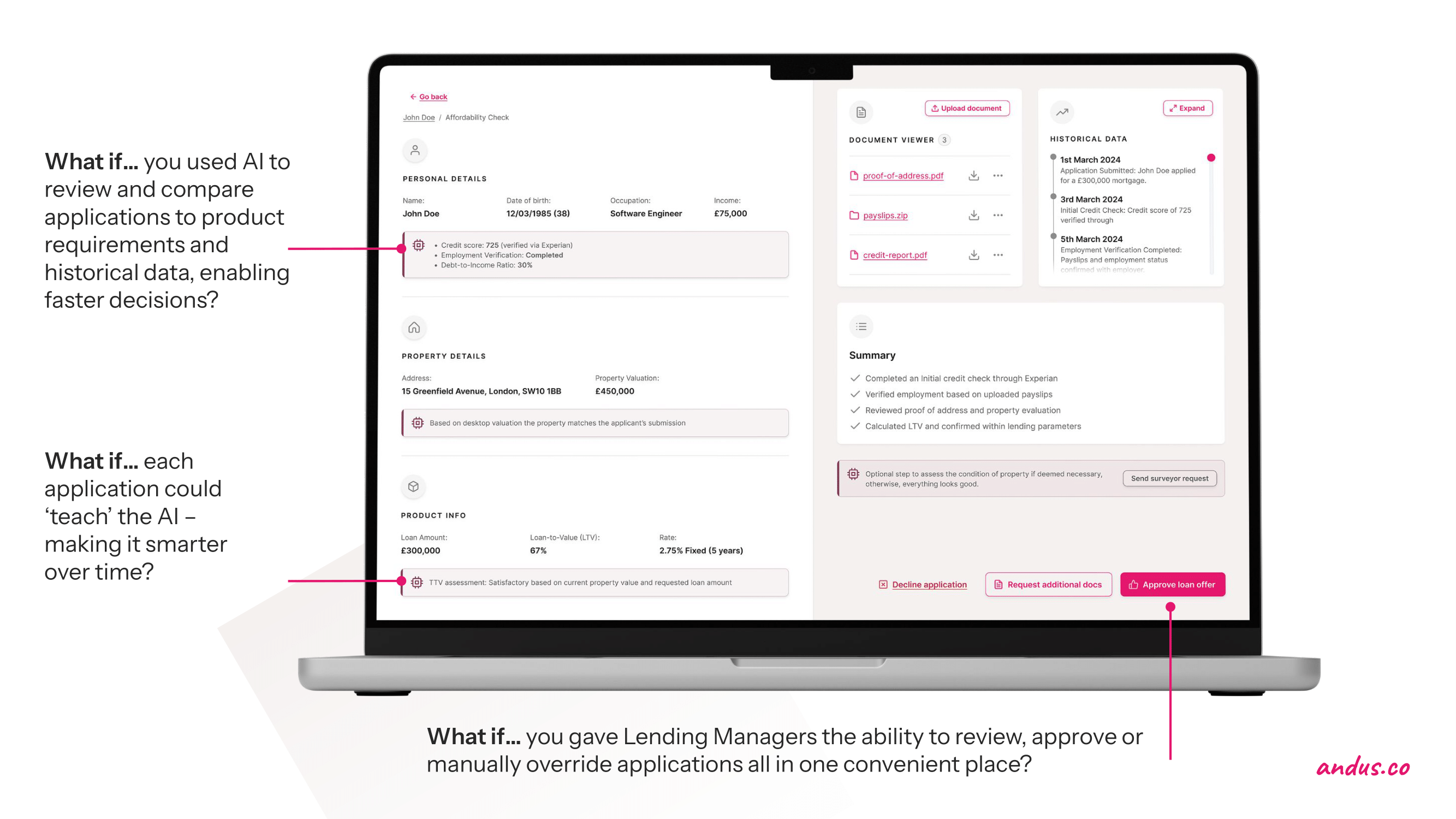

The (business) problem to solve

Customers aren’t the only ones struggling. The mortgage process is long and arduous for lenders, too. Applications usually take weeks due to resourcing issues and long, regulated processes that cause major bottlenecks. There is also a balancing act between automating what’s safe to automate and streamlining the human decision-making process.

The big question

How do you leverage AI as a daily co-pilot to allow your teams to review, and even approve, 10x the number of mortgage applications in a day?

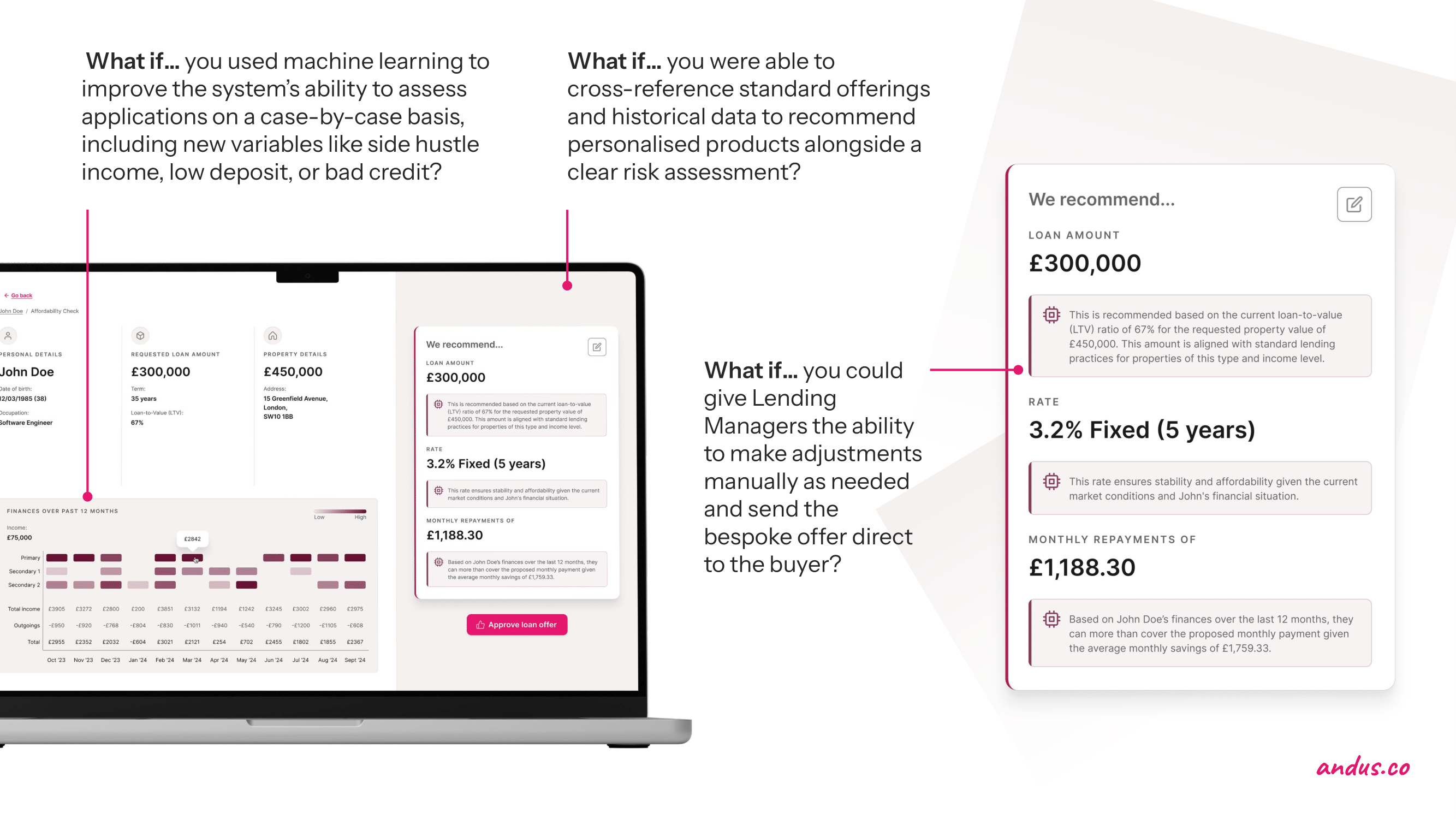

3. Seize the power of personalisation

With existing customers and new applications addressed, it’s time to broaden your horizons and think about the future. Explore how deeper personalisation – powered by AI – can open up remarkable new sources of opportunity.

The problem to solve

There are over 8,000 mortgage products – but no lender offers a complete set of options for all customer scenarios. As customer needs continue to shift and evolve, many valuable segments continue to go underserved.

Not only that, it also allows brokers to dominate the value chain as customers turn to them to help choose between the muchness of mortgages – costing lenders £1bn in commissions every year. AI creates the opportunity to serve customers tailored mortgage products on a deeper level, across a wider array of scenarios, and at a scale that’s not possible with human staff alone. The potential benefits include the ability to tap into a wider customer base, increase customer loyalty – and even cut out intermediaries all together.

The big questions

How do you use AI to meet emerging customer needs and a wider range of customer scenarios?

How can AI help you deliver more tailored advice, support and offers directly to customers so that they come to you first – and not a broker?

Where to next?

Where lenders find it particularly tough in this sea of opportunities, is knowing where to start. Afterall, radically improving the mortgage experience has its challenges, including the breadth of opportunities to choose from, the risk and regulations that make change daunting, and difficulty deciding which idea to invest in. These barriers are just some of the reasons why 79% of organisations don’t achieve their innovation goals.

So, how do you become one of the successful 21%? With a little help...

Where Ideas Grow.

As we like to say at &us, the key is to start by starting. This means choosing to make incremental progress towards your goal, and the &us Greenhouse is a great way to do this. It's a cost effective 2-4 week innovation programme designed to help you make progress faster.

Vesta Insights shakes up mortgages with AI

Veronica Breene, the founder of Vesta Insights discusses how a dataset of 50 million mortgages is helping create fairer lending for buyers, while reducing risk for lenders.

%201-min.png?width=1000&height=500&name=Blog-Header-%20Mortgage%20POV%20-%202000x1000%20(1)%201-min.png)

Improving the mortgage experience for the next generation

Millennial and Gen Z buyer behaviours are leading to increased mortgage innovation and competition for lenders. Find out how you should be adapting and what opportunities are emerging.

10 mortgage innovators to add to your watch list

The mortgage industry is at a turning point and these innovators are leading the way. See how organisations are leveraging automation, AI and UX design to improve the mortgage journey.