%201-min.png?width=1600&height=900&name=Blog-Header-%20Mortgage%20POV%20-%202000x1000%20(1)%201-min.png)

For Millennials and Gen Z, it's high time we shook up the mortgage experience.

We all know the mortgage process is notoriously stressful and difficult – with outdated paper-based processes, complicated jargon and strict qualifying processes. Despite its issues, this process has been the status quo for decades, with little innovation in the overall experience or mortgage products themselves. However, Millennials and Gen Z are here to shake up this status quo. As they enter the market, they're bringing with them new behaviours and values that guide their choices – causing a shift in consumer expectations.

This shift is creating mounting pressures for lenders to deliver smoother digital experiences and more flexible products that suit different lifestyle needs and priorities of younger buyers. Digital-first banks and new competitors are beginning to rise to this challenge by delivering seamless, tailored experiences across devices, and fixing clunky or paper-based processes plaguing the current mortgage experience. Established players, like legacy banks and building societies, urgently need to rethink their solutions in order to retain market share.

In this article, we’ve identified four opportunities to improve the mortgage experience and help lenders meet the evolving needs of a new generation of buyers.

Jump to a section:

- How buyers are changing

- The shifting competitor landscape

- The four opportunities

- How to get started with mortgage innovation

Buyer behaviours are changing

In the UK, we all know just how hard it is to buy your first home. In fact, England is the worst place in the developed world to find a home. Those Millennial and Gen Z buyers who are able to purchase a property are entering the market at a time where the cost of living is at an all time high. The result? Buying a first home requires more creativity and resourcefulness than ever – leading to some key behavioural changes in potential buyers.

Here are three important behavioural shifts:

Skimping and saving

Cash-strapped first-home buyers are changing their lifestyles to get on the ladder, with many living at their family home as long as possible to avoid spending thousands of pounds in the rental market.

DIY and renovation

Young buyers are now turning to TikTok and YouTube DIY tutorials to turn cheaper buys into their dream home. However, with the increasing cost of trade services and supplies, even saving for a renovation can feel out of reach.

Side hustles and portfolio careers

Post-pandemic behaviours towards work and the increasing cost of living have increased the number of people seeking additional income and flexibility, with more opting for portfolio careers (37% more than pre-pandemic), side hustles (over 65% of Millennials and Gen Z), and starting their own business (over 5% of over-16s in the UK).

Buyer values are evolving

In addition to changing behaviours, the core values of younger buyers are also shifting expectations in the mortgage market – changing how the average customer chooses their mortgage lender. Two important examples include:

1. Great (digital) expectations

Many Gen Zs and Millennials grew up during (or after) the rise of apps, so digital experiences and on-demand services are second nature. Expectations for these experiences are high and a core requirement of the products and services they choose – set by the frictionless, personalised digital experiences that have become standard.

2. Do no harm

Faced with a volatile and vulnerable world, younger generations increasingly have value systems based on trust and social good. They choose companies based on their ethics – with Millennials prioritising social issues (37%), followed by governance and environmental issues (both 24%).

The competitor landscape is shifting

Mortgage innovators are already jumping at the chance to solve these evolving customer needs, behaviours and values – syphoning them away from slow-moving banks and building societies who simply can’t adapt quickly enough. These innovators are disrupting the market in two key ways.

1. Challenger banks are expanding their offering to mortgages

In 2023, Starling acquired several mortgage portfolios and lent £4.9 billion. Monzo has also been in talks to make similar acquisitions, indicating that challenger banks are committed to capturing more of the mortgage market. The danger here for other lenders is that these digital-first banks strongly prioritise the customer experience, and already have a reputation for seamless, friction-free banking.

In fact, in a recent poll, it was found that customer trust of Starling, Monzo, and First Direct was 30% higher than for established banks like HSBC, TSB, and RBS – making them an already preferred provider for financial assistance.

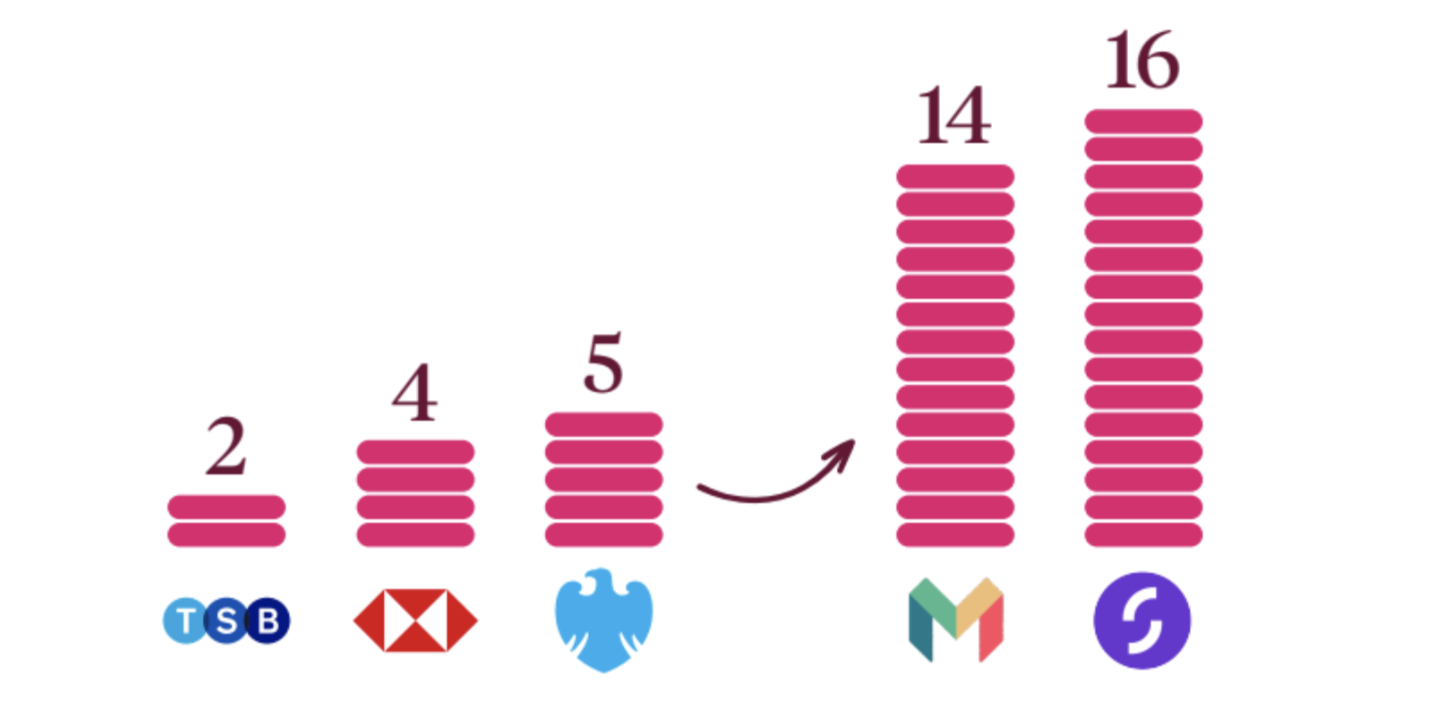

This is an even bigger threat to banks and building societies when considering challenger banks’ greater ability to adapt quickly to customer needs. Take a look, for example, at just how frequently Monzo and Starling update their apps in comparison to traditional banks.

Number of iOS app updates in the last 3 months (Mar 1-May 30 2024).

What this shows is how fast and responsive challenger banks are to customer needs and feedback, in stark contrast to traditional banks – where the lower update frequency indicates less focus on customer experience, and a slower pace of digital product innovation.

2. Newcomers are delivering innovative solutions to buyer pain points

Besides challenger banks themselves, new mortgage service providers are also capitalising on technology to serve up compelling customer-centric experiences that appeal to modern audiences. And they’re delivering all of this at incredible speed.

Examples of mortgage innovations from newcomers:

- Perenna is a mortgage provider focused on fixing the housing crisis and climate crisis in order to appeal to customer values. They’re also introducing new services by using covered bonds instead of savings deposits to further protect buyers.

- Habito has improved archaic processes by digitising and consolidating services across lending, legal processes, and property surveys. They’re seeing rapid growth by simplifying an otherwise complicated process in a seamless digital experience.

- Mojo Mortgages keeps brokering services free for buyers, while also offering personalised calls with their advisers. This taps into the needs of cash-strapped first-time buyers who need more advice.

Four mortgage innovation opportunities for lenders

To keep up with competitors and evolving customer needs, established lenders need to start innovating – rapidly. We’ve identified four innovation playgrounds, where lenders can experiment and test in order to bring new value to the next buying generation.

1. Outzag the competition on experience

Talking about a frictionless digital customer experience is far from groundbreaking - yet it remains both crucial for success, and still a challenge for many legacy lenders. The notoriously painful and long mortgage experience is no longer 'good enough' for the increasingly younger and digital-savvy buyer who may well be using 3-4 different apps to manage their finances. To stand out in this sea of companies, your technology, services, and staff need to live up to new industry standards and provide the best possible experience.

Across the entire mortgage experience, there is the opportunity to rethink and redesign every moment to be easier, faster and more intuitive.

This includes everything from helping customers understand processes to how mortgage application decisions might be accelerated. Take user experiences that are classically built around paperwork and long processes and reimagine what these moments could look like if done well.

Big questions:

- How do you rebuild a month-long process for a fast-moving audience that operates in seconds?

- How might you demystify parts of the process for buyers in the early stages of mortgage research?

2. Supercharge the struggling savers

Struggling savers need help getting out of the rental market and onto the ladder. In the wave of soaring property prices and looming interest rate rises, Millennials and Gen Z need to save as much as possible, as quickly as possible. This is no easy feat when rents have risen, forcing them to dedicate more income to rent rather than a deposit.

Consider how you could build long-term relationships with people saving for their first home by accelerating their house-buying goals.

Banks are in a particularly good position to seize this opportunity because the journey from saver to homeowner can be handled within one seamless journey. You can also look at how you can help first-home buyers break into the market sooner with special considerations.

Big questions:

- How can saving for a house be built into other banking or investment experiences?

- How could you build trust and understanding with your target customers in the early stages of saving?

3. Capture buyers with alternative finances

Instead of rejecting buyers with complex finances, build a system that caters to them. This is more nuanced than catering to the self-employed. Buyers with portfolio careers and diverse investments need lenders to recognise their income streams as valid. An example of these buyers are those who would rather have two or three side hustles to make their own way, while balancing bills with part-time work. This juggling act comes with an entrepreneurial mindset and often diverse finance sources, which may also encompass investments and crypto. Historically, the rigid approval processes of traditional lenders have provided little support to these buyers.

Catering your process to underserved individuals can help you reach an untapped segment of the market while freeing them from a maze of red tape.

Big questions:

- What is the biting point between offering a mortgage that works for the lender, but also fits diverse lifestyles and habits of buyers?

- How could you adapt your processes to simultaneously educate and engage these customers so they’re better prepared when they do want to buy their first home?

4. Power-up the renovators

Design mortgage solutions that accommodate budding renovators and DIYers. Properties that are ‘doer-uppers’ are the most popular Rightmove search amongst buyers, and home improvements account for the largest portion (22%) of major purchases across the UK. With so many people looking to get their hands on these properties, lenders have an opportunity to support first-time buyers who have renovation on their mind. Equally, an opportunity exists for lenders to help existing homeowners remortgage for renovation, to strengthen relationships and reduce the risk of losing them to another mortgage provider.

Providing a great remortgage experience, or offering options for renovations that push the boundaries of what’s on offer currently, can help you retain customers. For new home buyers, you can look at ways to support them with their first fixer-upper.

Big questions:

- Once home ownership is achieved, how can you help buyers unlock new value in their home with cash boosters to get that new kitchen or undertake the grand renovation?

- How could you tailor mortgage processes for new buyers looking to get straight into DIY and renovation?

How to get started with mortgage innovation

Discovering the motivations, habits and pain points of customers is essential in helping you understand opportunities for innovation – as well as validating a genuine need before time and effort is invested. Our services across innovation and transformation, including customer research and AX design, can help you adapt to industry changes and design innovative solutions to emerging opportunities.

Where Ideas Grow.

If you’ve got a particular challenge to tackle, or want to get your own innovation cycle moving, take a look at the &us Greenhouse. It's a cost effective 2-4 week innovation programme designed to help you make progress faster.

10 mortgage innovators to add to your watch list

The mortgage industry is at a turning point and these innovators are leading the way. See how organisations are leveraging automation, AI and UX design to improve the mortgage journey.

Vesta Insights shakes up mortgages with AI

Veronica Breene, the founder of Vesta Insights discusses how a dataset of 50 million mortgages is helping create fairer lending for buyers, while reducing risk for lenders.

Untapped mortgage innovation opportunities for lenders

There are so many opportunities to improve the mortgage experience. See our ideas for how to get started, including how you can use AI to streamline processes and build stronger customer relationships.